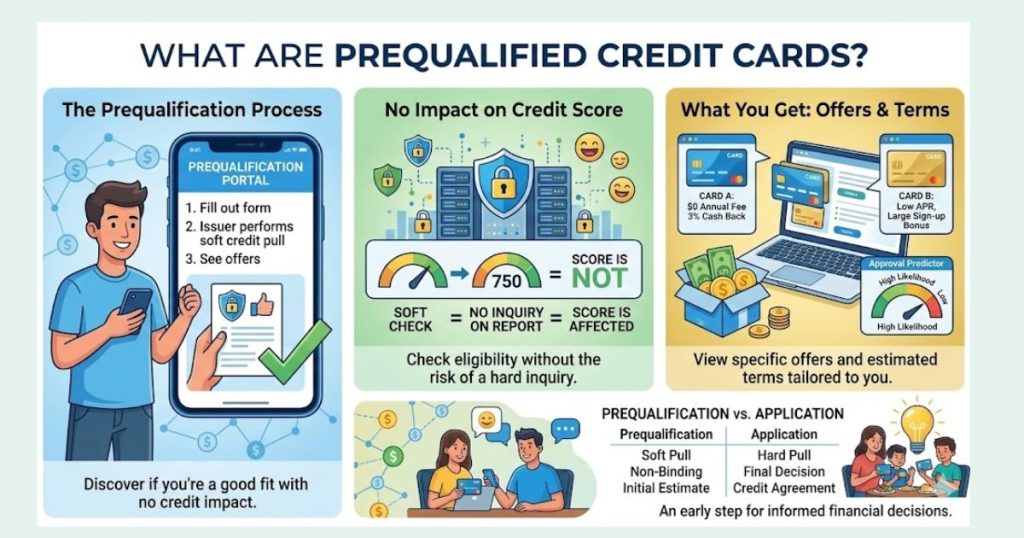

Applying for a credit card can be stressful, especially when rejection is a possibility. Prequalified credit cards offer a smarter approach. They let you check your chances of approval before officially applying, usually with a soft credit inquiry that won’t affect your credit score. This means fewer surprises, fewer rejections, and a better shot at approval.

These cards work by comparing your credit profile to the issuer’s requirements. Based on this, the issuer can provide an estimate of your approval odds without a hard credit pull. Many major banks offer pre-qualification tools online, letting you explore potential rewards, rates, and perks before committing.

Using prequalified credit cards strategically helps protect your credit, save time, and identify the best options for your financial goals. By understanding how pre-qualification works and applying wisely, you can increase your approval chances and get instant credit card approval, so it will work more effectively for you.

What Are Prequalified Credit Cards?

Prequalified credit cards are special offers you can see before officially applying. Lenders use limited information, often from a soft credit pull, to estimate your likelihood of approval.

It’s important to note: 👉 Being prequalified does not guarantee approval, but it does mean your odds are higher than average.

These offers commonly appear:

- On bank or credit card issuer websites

- Through online credit card comparison tools

- Via email or mail invitations

Because prequalification relies on a soft credit check, your credit score remains unaffected while you explore your options. Using prequalified credit cards wisely helps you target applications that match your profile, increasing your chances of approval and helping you make smarter credit decisions without risking your credit.

Prequalified vs Pre Approval Credit Cards

These terms are often confused, so here’s a clear breakdown:

Prequalified Credit Cards

- Typically, use a soft credit pull

- No impact on your credit score

- Shows estimated approval chances

- Still requires a full application for final approval

Pre-Approval Credit Cards

- Usually, a stronger signal than prequalification

- Still not a 100% guarantee of approval

- Final approval requires a hard credit inquiry

- Often based on more detailed credit and income data

Both prequalified and pre-approval credit cards let you gauge your chances without applying blindly. By using these tools, you can target applications more strategically, reduce unnecessary credit inquiries, and improve your odds of getting approved for the cards that fit your financial goals.

Why Checking Approval Odds Matters

Applying for the wrong credit card can cost more than just time it can impact your credit score. Every denied application:

- Triggers a hard inquiry

- Temporarily lowers your credit score

- Makes future approvals slightly harder

Using prequalified credit cards helps you avoid these pitfalls. They allow you to:

- Skip unnecessary credit hits

- Focus on cards you’re likely to be approved for

- Build or rebuild credit efficiently

- Apply with confidence instead of guessing

For anyone working on improving or establishing credit, checking your odds with prequalified credit cards is a smart, low-risk first step. It saves you money, protects your score, and guides you toward cards that match your financial profile.

Soft Pull Credit Card Pre-Approval: Check Your Approval Odds

A soft pull credit card pre-approval allows you to see if you’re likely to qualify for a credit card without affecting your credit score. Unlike a hard inquiry that happens during a full application, a soft pull simply reviews limited information from your credit report. Many lenders offer online pre-approval tools so you can check potential offers in seconds. This makes it easier to explore options and compare cards before submitting a real application.

Best Soft Pull Credit Card Pre-Approval Options

Several banks and credit card issuers provide soft pull pre-approval checks to help users find suitable credit cards. These tools show personalized offers based on your credit profile, income, and financial behavior. While pre-approval doesn’t guarantee final approval, it significantly improves your chances by matching you with cards that fit your credit range. Many people use these tools to discover rewards cards, cashback cards, or beginner credit cards without risking a hard inquiry.

Why Pre-Approval Credit Cards Are Useful

Using pre-approval credit cards helps you understand your approval odds before officially applying. This can protect your credit score from unnecessary hard inquiries and help you make smarter financial decisions. It’s especially helpful for people building credit or comparing multiple offers online. By checking pre-qualified offers first, you can focus only on credit cards that are more likely to approve you and choose the one that best fits your financial goals.

Who Should Use Prequalified Credit Cards?

Almost anyone can benefit from prequalified credit cards, but they’re particularly useful if you:

- Have fair or average credit and want to check approval odds safely

- Are you rebuilding credit after missed payments or financial setbacks

- Recently applied for multiple cards and want to avoid extra hard inquiries

- Aren’t sure where your credit stands

- Want to minimize the risk of unnecessary rejections

Even individuals with excellent credit often use prequalified credit cards to save time, compare offers, and protect their credit score. By checking prequalification first, you can focus your applications on cards that match your profile, improving your chances of approval and making smarter credit decisions.

Where to Find Prequalified Credit Card Offers

Finding prequalified credit cards is easier than you might think. Many major issuers, comparison platforms, and even mail or email offers let you check your approval odds safely with a soft pull. Knowing where to look helps you target the right cards and improve your chances.

Major Credit Card Issuers

Most big banks provide online prequalification tools. Enter basic info like your name, address, last 4 digits of your SSN, and income range. Results appear instantly without affecting your credit score. These tools are a quick way to discover prequalified credit cards that match your financial profile.

Credit Card Comparison Platforms

Trusted comparison websites show cards tailored to your profile using soft pulls. They’re ideal for comparing rewards, discovering no-annual-fee cards, and spotting prequalified credit cards with the best benefits for your spending habits.

Mail and Email Offers: Some preselected offers arrive via mail or email, often based on soft credit data. While convenient, always read terms carefully to confirm benefits and eligibility before applying.

What Information Affects Prequalification Results?

Even though prequalified credit cards rely on a soft pull, lenders still consider key factors to estimate your approval odds. Understanding these can help you improve your chances before applying.

- Credit Score Range: Your credit score influences which prequalified credit cards you see, potential credit limits, and estimated interest rates. A higher score typically unlocks better offers.

- Payment History: Late or missed payments can lower your approval odds, even for prequalification offers. Keeping a clean history helps you access more card options.

- Credit Utilization: High balances relative to your limits can hurt your chances. Maintaining low utilization improves your prequalification results and overall credit health.

- Length of Credit History: New credit profiles may see fewer offers, but they aren’t excluded. Over time, building a solid credit history opens up more prequalified credit card opportunities with better rewards and benefits.

Common Myths About Prequalified Credit Cards

- Prequalified means guaranteed approval

Not true. Prequalification indicates higher odds, but final approval still requires a full application and sometimes a hard pull. - Soft pulls hurt your credit

Incorrect. Checking prequalified credit cards uses a soft inquiry, which does not affect your credit score. - Only people with good credit get prequalified

False. Lenders offer prequalification options for fair or rebuilding credit, making it accessible to more applicants. - You should apply to every prequalified offer

Not recommended. Strategically choose the card that best fits your spending habits and financial goals to maximize approval chances and benefits.

Using prequalified credit cards wisely can save time, protect your credit, and improve your odds of approval. Don’t fall for these common myths.

How to Improve Approval Chances Before Applying

Want to increase your odds with prequalified credit cards? Follow these steps:

- Lower Your Credit Utilization: Keep balances below 30% of your credit limits to improve prequalification results.

- Check Your Credit Report: Correct any errors that could affect your estimated approval odds.

- Avoid Multiple Applications: Don’t apply for new credit for 30–60 days before checking prequalified offers.

- Update Income Information: Accurate income details ensure better matches with card limits and offers.

- Pick the Right Cards: Focus on prequalified credit cards that match your credit profile, whether you’re building, rebuilding, or maintaining credit.

Even small steps can make a big difference, helping you access stronger offers, higher limits, and better rewards—all while protecting your credit score during the prequalification process.

Best Types of Prequalified Credit Cards to Consider

Depending on your goals, certain prequalified credit cards may be a better fit for you:

- No Annual Fee Cards: Perfect for long-term use and building credit without worrying about yearly fees. These cards provide steady benefits while keeping costs low.

- Cashback Credit Cards: Ideal for earning rewards on everyday spending like groceries, gas, or dining. Prequalified offers help you find cards that match your habits and maximize cashback.

- Low Credit Score Cards: Designed for fair or limited credit histories. These prequalified options give you a better chance of approval and help rebuild or establish credit.

- Secured Credit Cards: Some secured cards offer prequalification, too. They require a deposit but are excellent stepping stones for building a stronger credit profile and unlocking better future card options.

What Happens After You Apply?

Once you select a prequalified credit card and submit your application, the issuer performs a hard inquiry to review your full credit profile. Based on this detailed check, you’ll typically receive instant or near-instant results. If approved, your new account will be opened, and you can start using your card right away. If denied, no account is created, but the hard inquiry remains on your credit report, which is why it’s important to apply strategically and only for cards where prequalification indicates strong approval odds.

Sum Up

Applying blindly can hurt your credit, but prequalified credit cards let you approach applications with strategy and confidence. By checking approval odds through soft pull cards, reviewing offers that match your credit profile, and using pre-approval options wisely, you protect your score while improving your chances of success. Smart credit users apply thoughtfully, not recklessly, avoiding unnecessary denials and hard inquiry hits. Prequalification helps you focus on cards you’re likely to get, whether for rewards, building credit, or low-fee options.

Start with prequalified credit cards today, apply strategically, and watch your credit grow safely. A little planning now means stronger credit opportunities in the future and fewer surprises along the way. For more tips on building credit responsibly, check out the best credit cards for bad credit.

Leave a Reply